Financial goals can often seem large and overwhelming. But don’t be intimidated! Start with small and fun financial goals to build confidence and momentum toward larger goals. Not sure how to start? Here are some tips on how to choose a small and fun financial goal to get started.

Make a list of potential financial goals

Start by making a list of potential financial goals. Be creative when you make this list! You can start with the usual suspects like a retirement fund or a college fund for the kids, but don’t stop there. Is there a hobby you’ve wanted to try but haven’t had the cash to get started? Or maybe a trip you’ve wanted to go on but haven’t had the funds? Write those down!

A financial goal is more than just building up wealth, it’s about making choices with the money that you have. Paying down debt or saving for the future are great financial goals, but so is learning an instrument or giving meaningfully to a good cause. Think creatively about your financial goals and you’re more likely to find one you’ll really stick with.

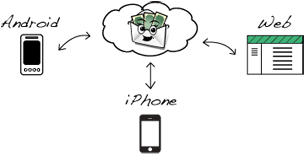

Did you know you can sync your EEBA household across multiple mobile devices and the web?

Did you know you can sync your EEBA household across multiple mobile devices and the web?

Anyone who’s tried, knows. Sitting down to talk about money can be stressful. Whether it’s a spouse, a child, a dependent parent, or even a roommate, our lives –and our money– are interwoven with those around us, and with that comes conflict. We enter conversations about money with the best of intentions, but often leave frustrated or even resentful.

Anyone who’s tried, knows. Sitting down to talk about money can be stressful. Whether it’s a spouse, a child, a dependent parent, or even a roommate, our lives –and our money– are interwoven with those around us, and with that comes conflict. We enter conversations about money with the best of intentions, but often leave frustrated or even resentful.